A Power Combo: High MPR for Overseas Spend + Lounge Access

Overview

| Version |

UOB VI

UOB VI

|

UOB VI PB

UOB VI PB

|

| BolehMiles Rating |

Boleh / |

Boleh / |

| Miles Per Ringgit (MPR) |

0.83 MPR (Overseas Spend) 0.41 MPR (Dining, ≥ RM1000) 0.08 MPR (Others) |

1.00 MPR (Overseas Spend) 0.50 MPR (Dining, ≥ RM1000) 0.08 MPR (Others) |

| FFPs | Enrich, KrisFlyer, and Asia Miles | Enrich, KrisFlyer, and Asia Miles |

| Lounge Access |

12 x Per year Worldwide Access to ~1500 Lounges ➤ See Lounge List |

12 x Per year Worldwide Access to ~2300 Lounges ➤ See Lounge List |

| Other Perks | 12x Limo to KLIA T1 or T2 Visa Infinite Benefits |

12x Limo to KLIA T1 or T2 Visa Infinite Benefits |

| Requirement | RM120k p.a income | RM120k p.a income & RM500k AUM or RM 1 Million AUM |

| Annual Fee | RM600 for primary cardholder RM300 for supplementary cards |

Free |

| Welcome/ Renewal Bonus |

None | None |

| Payment Network |

Visa Infinite | Visa Infinite |

| Terms& Conditions |

Link to T&C here. | Link to T&C here. |

|

🎁 Apply now and get RM88 Cashback + 1 year annual fee waiver.

T&Cs apply

|

||

Believe it or not, UOB actually has three versions of the Visa Infinite cards, which can be a bit confusing. There’s the standard UOB VI (for the mass market), the UOB VI Privilege Banking (for those with RM500k AUM), and lastly the UOB VI Metal (for the Datuks who like to collect metal cards as paperweights). All three cards are positioned for Overseas Spend.

For this review, we’ll focus only on the UOB VI and the UOB VI Privilege Banking versions. We’ll leave the UOB VI Metal for another post.

The base UOB VI earn 0.83 MPR for Overseas Spend, while the UOB VI PB gets a slight boost at 1.00MPR. They also double as dining cards. If you spend at least RM1,000 on dining monthly, the UOB VI earns 0.41 MPR, while the PB version earns 0.5 MPR, both in Meat Miles (KrisFlyer and Asia Miles).

Beyond that, the two cards are largely similar. We’ll break down the details for you below.

Who is this card for?

The UOB Visa Infinite cards are best suited for frequent flyers. For both business and leisure travels, the card fits well into your wallet.

But what if you don’t travel that often? Yes, you can still get value out of it. Any time you’re paying in foreign currency online be it subscriptions, flights, hotels, or online shopping, you still earn the 0.83 or 1.00 MPR.

It’s also useful for Malaysians living abroad. Take Singapore for example, you can treat the UOB VI as a general spending card with ~2.57 MPD, and UOB VI Privilege Banking earning a better 3.1 MPD (based on ~1 SGD ≈ RM3.1 at the time of writing).

Miles Earning Rate

At 0.83 MPR for the UOB VI and 1.00 MPR for the UOB VI PB on overseas spend, these are among the highest MPR rates earn rates in the Malaysian market.

Personal Banking

| Card | Category | Miles per Ringgit (MPR) |

|---|---|---|

|

UOB VI

|

Overseas Dining |

0.83 Overseas/ 0.41 Dining KrisFlyer & Asia Miles |

UOB PME

UOB PME

|

Overseas | 0.83 Overseas/ 1.00 (SGD, IDR, THB, VND) KrisFlyer & Asia Miles |

CIMB Travel World Elite

CIMB Travel World Elite

|

Overseas Airlines Duty-Free |

0.80 Enrich/ 0.67 Alt Miles |

Maybank WEM

Maybank WEM

|

Overseas | 0.40 Overseas KrisFlyer & Asia Miles |

The base UOB VI earns the same 0.83 MPR as the UOB PME for Overseas spend. The PME does have the edge with its boosted 1.0 MPR on 4 ASEAN currencies, so it’s clearly a better pick from the miles earning rate perspective.

It’s not easy to pick between the UOB VI and UOB PME. The DragonPass is tempting, sure… but you give up on the 1.0 MPR for selected currencies and those RM80 Grab ride home vouchers. At the end of the day, it really comes down to which one is more practical for you.

If you prefer earning some Seafood Miles (Avios, Flying Blue, EVA, etc) for the flexibility, then the CIMB TWE (and the CIMB ecosystem) is the stronger option. The MPR is slightly lower, but you’re also paying lower FCY fees, and you gain much flexibility across multiple FFPs and hotel elite programs.

Privilege/Preferred Banking

Privilege, Preferred, Priority, Premier banking… they’re all essentially in the same market with RM250k to RM500k AUM requirement. With SCB Beyond and HSBC Premier entering the space lately, it’s getting more competitive to cater to everyone wants to feel a bit more “atas” nowadays.

| Card | Category | AUM | Miles per Ringgit (MPR) |

|---|---|---|---|

|

UOB VI PB

|

Overseas Dining |

RM500k | 1.00 Overseas/ 0.50 Dining KrisFlyer & Asia Miles |

CIMB Preferred VI

CIMB Preferred VI

|

Dining Overseas |

RM250k | 0.92 Enrich/ 0.76 Alt Miles2 |

SCB Beyond

SCB Beyond

|

Overseas Overseas Dining & Shopping Krisflyer & Asia Miles |

RM300k | 0.71 Overseas/ 1.42 Overseas Dining & Shopping Krisflyer & Asia Miles |

HSBC Premier World

HSBC Premier World

|

Overseas1 (Physical only) |

RM300k | 0.75 Seafood/ 1.00 KrisFlyer & Asia Miles |

2 CIMB Preferred VI: 0.76 MPR assumes bonus with RM10,000 spend. Rate drops to 0.74 MPR with RM8,000 spend.

For Privilege Banking customers with RM500k AUM, the choice between UOB VI PB and UOB PME becomes much clearer.

The UOB VI PB earns 1.0 MPR on all foreign currency spend, not just the selected ASEAN currencies like the UOB PME. So the UOB VI PB is the better pick over UOB PME here.

Now, there are also CIMB Preferred VI, SCB Beyond and HSBC Premier World in this space. They come with much lower AUM requirements compared to the UOB VI PB, but with lower MPR.

The CIMB VI Preferred is perhaps the most well balanced pick among the 3, but then you will have to keep track of your total monthly spend. The SCB Beyond looks the strongest on paper with 1.42 MPR, but it’s limited to Overseas Dining and Shopping.

The HSBC Premier World is a bit restrictive, only rewarding physical transactions, but if you still swipe in person often, it can still be a decent pick.

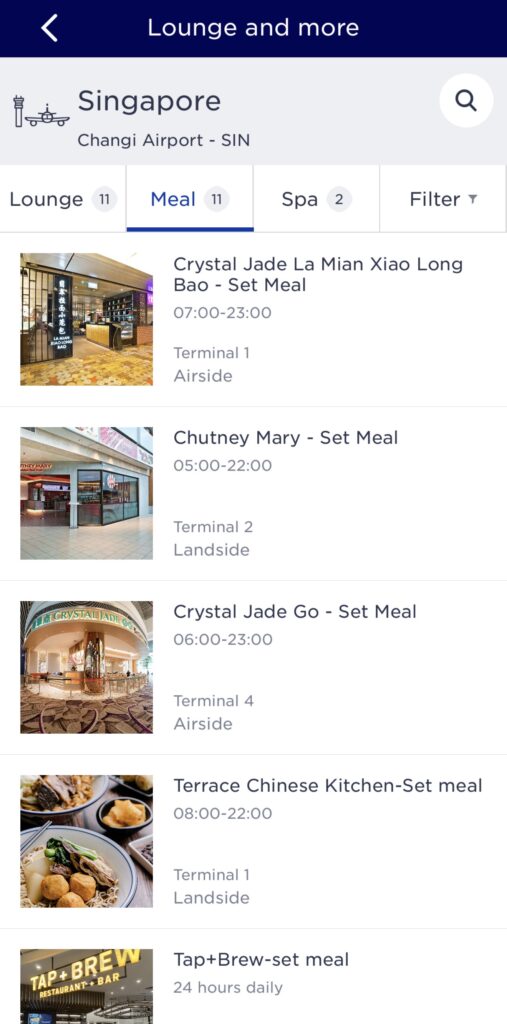

Lounge Access

Both the UOB VI and UOB VI Privilege Banking cards come with 12x DragonPass lounge visits worldwide. for the primary cardholder only. Supplementary cardholders get no access.

The UOB VI is currently the only mass market card in Malaysia offering DragonPass, much better than other “Plaza Premium cards” with wider network of lounge selection, restaurants, spas, and even sleeping spots.

Here are some examples from the DragonPass Travel Companion app for Restaurants in Singapore.

Here’s a breakdown of the types of establishments you can access with DragonPass worldwide.

| Category | UOB VI |

UOB VI PB |

|---|---|---|

| 🛋️ Lounge | 755 | 1,477 |

| 🍽️ Restaurant | 724 | 827 |

| 💆 Spa / Massage | 8 | 42 |

| 😴 Sleep / Rest | 13 | 24 |

| 🌍 TOTAL | 1,500 | 2,370 |

⚠️ Figures may change over time. Refer to Dragonpass Airport Companion App for the latest info.

Interestingly, the UOB VI Privilege Banking version gives you access to 800+ more lounges compared to the standard UOB VI.

That said, even at 1,500, the UOB VI is already attractive in terms lounge access selection.

Another interesting thing about the UOB VI Privilege Banking version is that it still gives you access to lounges at KLIA T2, even though UOB has removed KLIA T2 access for most of its other travel cards since Aug 2025.

Also, as with other UOB cards, you’ll get access to a dedicated UOB section at Plaza Premium Lounge (KLIA T1). That said, with all that interesting restaurants and sleep spots above, you might want to keep your DragonPass quota and not use it in Plaza Premium lounges.

Foreign Currency Transaction Cost

Based on past data points, the UOB FCY fee is roughly ~2.25% on top of Visa FX rates, and may fluctuate based on market conditions.

In other words, the cost of miles for UOB VI is 2.55CPM, and the UOV VI PB is 2.25CPM. The CPM rates seem reasonable value propositions, as we value Krisflyer Miles at 5 to 10 CPM.

Other Perks

Ride to Airport: The card offers a Complimentary Ride to Airport with minimum spend of RM5000 on selected MCCs (Hotels, Airlines and Travel Agencies). The Limo must be booked within 30 days from the earliest date of transaction on the selected MCCs. There is a cap of 12 redemptions a year and 2 redemptions per month. Additionally, there is also a shared pool of 7000 redemption quota for all UOB cardholders until Dec 2026.

Insurance: The card also comes with decent complimentary insurance, with coverage of up to RM500,000 provided by Liberty Insurance. You can check out our review of the different credit card travel insurance options here.

Visa Infinite Perks: You automatically enjoy Visa Infinite perks listed on this website. There are some gems here such as 14% discount on Agoda and other hotel benefits.

Exclusions

The full list of exclusions for this card can be found in the terms here.

Notable exclusions are Petrol, Transportation and Utility payments. UOB did not provide the list of excluded transportation MCCs, so it’s best to avoid using this card for trains and ride hailing overseas.

Is the annual fee worth it?

The UOB VI comes with a RM600 annual fee. Right now, UOB is offering a 1-year fee waiver for new cardholders until 31 Dec 2026.

For the UOB VI Privilege Banking version, the annual fee has been permanently waived since Jul 2025.

Based on our own rough estimation below, the total value you can extract comes up to around RM810. This assumes you fully utilise all 12 DragonPass visits in a year.

If 12x Dragonpass is too much for you, no worries, you can try hitting multiple establishments in a single trip (a.k.a lounge hopping / lounge safari).

| Perk | Valuation | Value |

| Lounge Visit | Assuming 12 visits per year and assigning RM50 per visit. Hence RM50 x 12 = RM600 | RM600 |

| Airport Limo | Assume that we only take it twice a year and assign value of RM80 (slightly higher than Grab cost). Hence RM80 x 2 = RM160 | RM160 |

| Travel Insurance | Assume the cost of an annual insurance of RM50 per year | RM50 |

| Total 💼 | RM810 | |

Conclusion

Overall, both UOB VI versions are rated “Boleh.” You’re getting strong MPR, a solid mix of lounge access, and limo rides to the airport. It also doubles as a Dining card with 0.41 / 0.50 MPR with minimum spend of RM1000 each month.

The main downsides are the exclusion on transportation spend (geez UOB… isn’t this a travel card?), and you’ll need to hit RM5,000 minimum spend on eligible transactions to unlock the Limo benefit.

The UOB VI is a staple in our 2026 Best Credit Cards for Miles post. We’d recommend having either this or the UOB PME in your miles card portfolio.

But should you pick this over the UOB PME, or just hold both cards? We’ll break that down in a separate comparison post. For now, that wraps up this review.

If you’re new to BolehMiles, be sure to join us on our Telegram below.